Analysis Prepared and Written by Jared Walczak

Twelve years after North Carolina embarked on the first of several rounds of pro-growth tax reform, the state now boasts a 3.99% flat individual income tax, a 2.0% corporate income tax, reduced business exposure to the corporate franchise tax, and the economic results to show for it. North Carolina’s population has grown 66% faster than the national average since 2013. The state has added 1.1 million jobs since 2013, growing 40% faster than the national average. And gross state product has risen 24% faster in North Carolina than in the U.S. as a whole. North Carolina’s tax reforms have been a rousing success.

Now, however, policymakers are divided on a vexing question: will the additional revenue trigger-based individual income tax rate reductions, as adopted in 2023, enhance the state’s competitiveness and contribute to further economic growth, or could they overreach, undermining the remarkable achievements of the past twelve years?

The eventual target, a 2.49% flat-rate individual income tax, would further enhance North Carolina’s tax competitiveness, resulting in what would currently be the lowest top or single-rate individual income tax rate in the country. Given North Carolina’s successes to date, there is reason to believe that this target is in reach. The triggers adopted in 2023, however, are a poor way to get there.

Will the additional revenue trigger-based individual income tax rate reductions, as adopted in 2023, enhance the state’s competitiveness and contribute to further economic growth, or could they overreach, undermining the remarkable achievements of the past twelve years?

Well-designed triggers make future rate reductions contingent on revenue availability. These triggers are, in that sense, barely revenue triggers at all, as their benchmarks are not meaningfully tied to the state’s ability to afford the reductions. They have the potential to implement rate reductions at the wrong time, giving lawmakers an unenviable choice: cancel or reverse a tax cut, or risk an avoidable budget shortfall. If the triggers are perceived as failing, moreover, that failure could derail future reforms. Tax reformers would be well advised to revisit the current trigger design to prioritize sustainable relief that locks in the gains of more than a decade of pro-growth tax reform.

North Carolina’s Revenue Triggers are Poorly Designed

With the flat income tax rate trimmed to 3.99% as of January 1, 2026, further reductions are to be implemented in 0.5 percentage point increments, subject to the state meeting statutory general fund revenue targets. The triggered reductions will run between tax years 2027 and 2034, or until the rate reaches 2.49%, whichever comes first.

Unlike tax triggers in most states, North Carolina’s triggers employ static benchmarks. The 2027 tax rate will be cut, for instance, if net general fund revenues exceed $33.042 billion in FY 2027 (ending June 30, 2026), and the 2028 tax cut is contingent upon FY 2028 net general fund revenues eclipsing $34.1 billion. While the revenue targets escalate in an implicit acknowledgment of inflation and population growth, they do not incorporate dynamic adjustments for either. That is a particularly salient omission in a high-inflation environment and in a state that—thanks in part to the success of prior tax reforms—continues to experience robust population growth.

The pending triggered reductions represent North Carolina’s first effort to reduce individual income tax rates subject to revenue availability, as all prior individual income tax rate reductions were implemented immediately or according to an established schedule, rather than being tied to achieving specific revenue targets. They are not, however, the state’s first experiment with tax triggers.

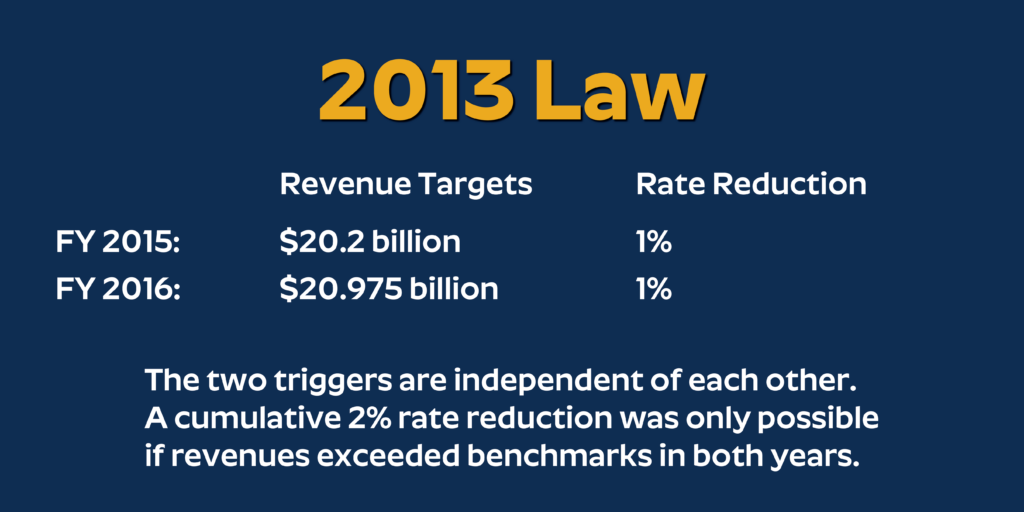

The original 2013 tax reform legislation featured revenue triggers to implement two step-downs in the corporate income tax rate. These triggers also featured static, statutorily set revenue targets. Originally, the law provided for a 1 percentage point rate reduction if FY 2015 net general fund revenues exceeded $20.2 billion and a further 1 percentage point reduction if FY 2016 collections exceeded $20.975 billion.

The two triggers were independent of each other. A 1 percent rate cut was possible either if the first-year benchmark was met but not the second, or, alternatively, if the second-year benchmark was met even though the first was missed. A cumulative two percentage point reduction, however, was only possible if revenues exceeded both benchmarks in successive years.

Lawmakers ultimately recognized and corrected the flaw in this design: tying the benchmarks to specific, sequential years required extraordinary growth in the second year, providing no breathing room after absorbing the revenue reduction associated with the initial rate cut. In 2015, lawmakers stripped the requirement that the second revenue target be met in FY 2016, permitting a subsequent rate reduction whenever collections exceeded $20.975 billion.

That revision reversed the stinginess of the original triggers, replacing them with a soft target: given inflation, collections were virtually guaranteed to exceed $20.975 billion eventually, even if revenues were weak. The risk here was modest, as corporate income taxes raise far less than individual income taxes, and the state’s economic growth was robust. The 2013 and 2015 decisions, however, offered a preview of the design of the individual income tax triggers adopted in 2023. The current triggers combine the 2013 legislation’s focus on hitting targets in specific years with the 2015 revisions’ elevated risk of triggering reductions in the absence of real growth.

In 2015, lawmakers stripped the requirement that the second revenue target be met in FY 2016, permitting a subsequent rate reduction whenever collections exceeded $20.975 billion.

North Carolina’s Revenue Targets are Poorly Calibrated

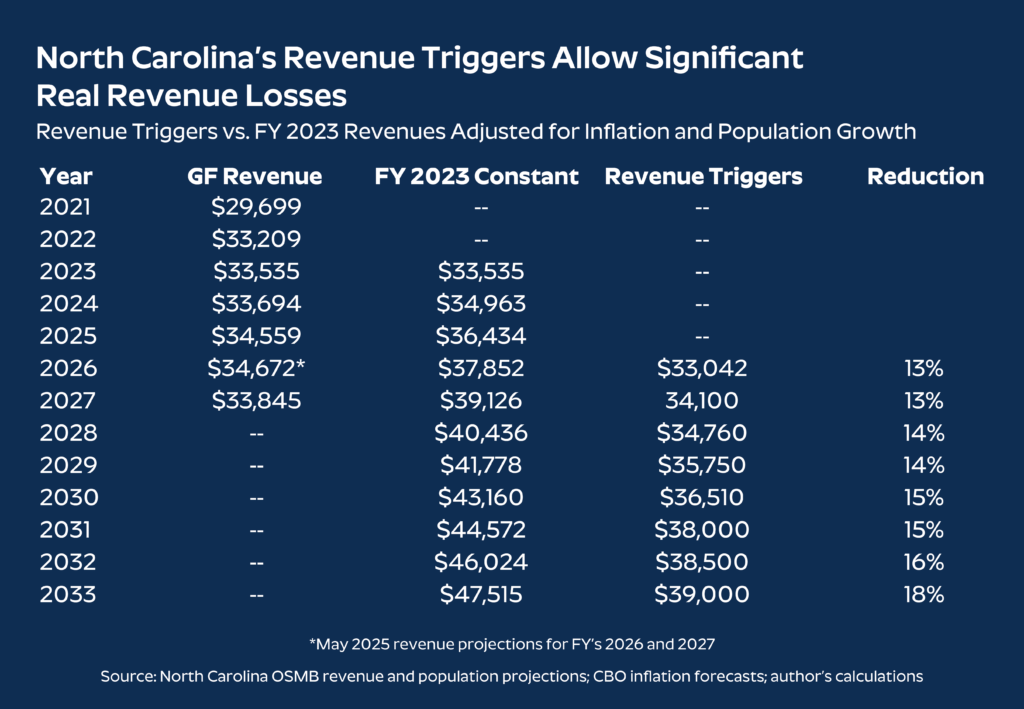

North Carolina generated $34.56 billion in general fund revenues in FY 2025, with forecasters anticipating slower growth—even declines in real terms—in the current biennium. The most recent forecast, the May 2025 revision, projects $34.67 billion in FY 2026, enough to trigger the first reduction to 3.49%. Largely because of this rate reduction, the Office of State Management and Budget (OSMB) anticipates FY 2027 revenues of $33.84 billion. That would represent a decline in nominal, to say nothing of real (inflation-adjusted) terms, but also an amount just a hair below the $34.1 billion necessary to initiate the second triggered rate reduction, to 2.99%.

When the current triggers were adopted in 2023, the most recent fiscal year had yielded $33.54 billion in general fund revenue. The threshold chosen to trigger a rate reduction three years later ($33.04 billion) was $500 million below FY 2023 collections in nominal terms, signaling lawmakers’ willingness to reduce the size of government, not just forego a share of future revenue growth. At the time, North Carolina was looking ahead to additional statutorily defined income tax rate phase-downs to 3.99%, and the trigger thresholds effectively permitted the state to continue cutting rates even if revenues remained lower (even in nominal terms) after those reductions.

This was highly unusual in and of itself. But the subsequent triggers are even more aggressive. A final rate cut could be triggered for tax year 2034 if FY 2033 revenues exceed $39 billion. Using FY 2023 revenues as a base year, FY 2033 receipts of $47.52 billion would be necessary for a no-growth scenario after adjusting for inflation and population growth. Only generating $39 billion in FY 2033 would represent an 18% decline in real collections per capita—and would still be enough to trigger a final rate reduction.

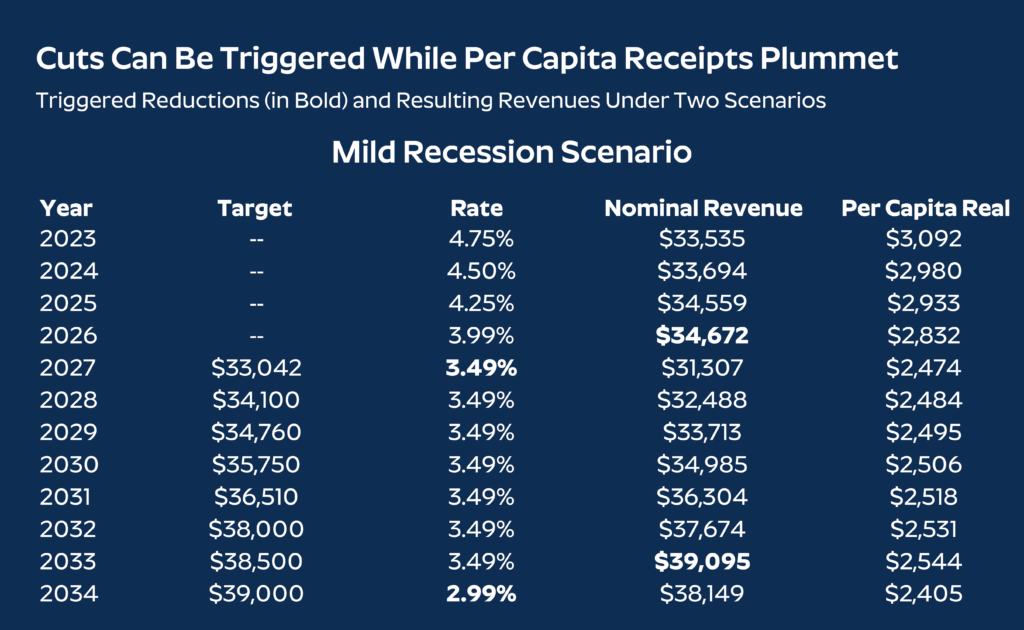

The table below shows actual general fund revenues for FYs 2021-2025 with current forecasts for FYs 2026-2027, alongside base year collections adjusted for projected annual inflation and population growth through FY 2033. Finally, these figures are compared to the amounts specified in statute for triggered rate reductions, and the per capita revenue reduction (compared to baseline) the state could experience and still meet the next trigger.

The current triggers were adopted during a period of high inflation. Had the rate of inflation remained at historical averages since their adoption, the real value of the first trigger would likely be over $1 billion higher than it is under current projections. Even that amount, however, would be highly contractionary.

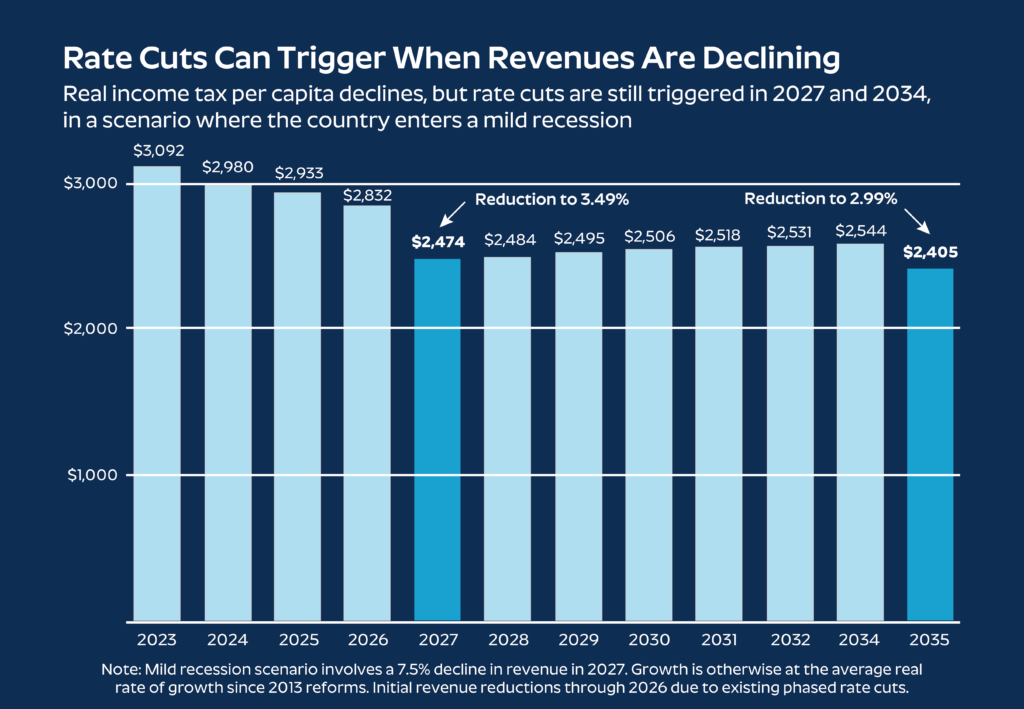

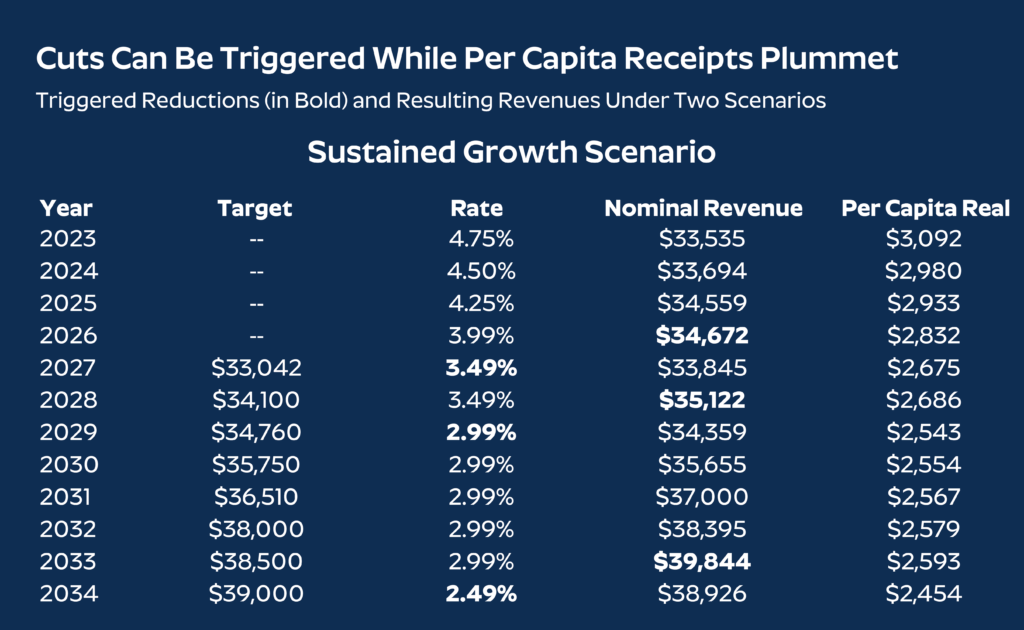

For a sense of how the current triggers could play out, imagine a scenario where North Carolina personal income continues to increase at its real average rate of growth since the 2013 reforms. In FY 2026, revenues would be sufficient to trigger the initial rate reduction, to 3.49%, for tax year 2027. The cost of this tax cut would be enough to delay the next reduction (to 2.99%) until tax year 2029, and that reduction would put the state far enough back that the next trigger’s threshold wouldn’t be met until the final year (FY 2033), yielding a tax cut to 2.49% for the 2034 tax year.

Nominal revenues for 2034 would be $38.93 billion, the inflation and population-adjusted equivalent of $22.88 billion in 2023, when the triggers were adopted, and when actual collections were $33.54 billion. In constant 2023 dollars, per capita revenue would decline from $3,092 to $2,454. Alternatively, imagine a scenario where the country slid into recession in FY 2027, shortly after the first trigger (based on FY 2026 revenues) was met. Assuming North Carolina grew out of the recession at current growth rates, revenue could slide as much as 7.5 percentage points in FY 2027 and the state would still trigger another rate cut by FY 2033 with revenues 16 percentage points lower than the inflation- and population-adjusted figure for FY 2025.

Assuming North Carolina grew out of the recession at current growth rates, revenue could slide as much as 7.5 percentage points in FY 2027 and the state would still trigger another rate cut by FY 2033 with revenues 16 percentage points lower than the inflation- and population-adjusted figure for FY 2025.

Note: Trigger revenue targets and resulting rate reductions are in bold. Mild recession scenario involves a 7.5% decline in revenue. Growth is otherwise at the average real rate of growth since the 2013 reforms.

Source: State statutes; state revenue data; author’s calculations.

The uncertainty created by the triggers currently on the books, and the unplanned spending cuts they could force, undermines the state’s pro-growth goals. Tax competitiveness promotes economic growth, but uncertainty creates jitters, and budget crises would make the state less attractive for businesses and individuals.

It is possible, of course, that North Carolina’s economy will grow at a pace that is sufficient to cover the costs of the rate reductions. In that case, the triggered reductions would do no harm, because revenues would be so much higher than what is necessary to yield a rate cut. But the possibility of such a happy accident should not drive policy. If North Carolina proves able to afford rate reductions to 2.49% by 2034, which would require annual economic growth of nearly 6 percent per year, the state could achieve the same outcome with more responsible triggers.

North Carolina’s Revenue Reserves Can’t Save the Triggers

Malfunctioning triggers could force lawmakers to tap the state’s rainy day funds, but revenue reserves are designed for short-term shocks, not long-term policies. Even a year’s worth of buffer would cut deeply into the states’ savings.

North Carolina has multiple revenue reserves, some of which are restricted for certain purposes. The principal funds are the Savings Reserve, a traditional rainy day fund designed to help the state weather revenue losses or budget shortfalls, and the Stabilization and Investment Reserve, a repository for additional savings from the pandemic era that is intended to be drawn down, not saved for a revenue crisis.

Taken together, the Savings Reserve ($3.62 billion) and the Stabilization and Inflation Reserve ($0.84 billion) stand at almost precisely 15% of prior general fund operating budget appropriations as of November 2025, with the Savings Reserve itself at 12.16%. This is marginally ahead of the 11.9% target calculated by the Office of State Budget and Management under state law.

Historically, many experts recommended revenue reserve targets as low as 5%. However, experts have increasingly identified 15% or two months’ operating budgets (about 16.7%) as best practice, a target that has been more widely embraced post-pandemic. North Carolina is in this range when taking both major reserve funds into account, but the Stabilization and Investment Reserve is meant to be drawn down and may not be available for any future shortfalls. Ideally, policymakers should target at least 15% in the Savings Reserve itself. And while reserves can help navigate revenue uncertainty while implementing tax reforms, one-time reserves cannot be relied upon as a long-term solution for overly aggressive rate cuts.

Conclusion

North Carolina has thrived under years of tax reform, and the goal of a 2.49% flat income tax rate—a hair below the current lows of 2.5% in Arizona and North Dakota—is commendable and, in time, attainable. Lawmakers, however, should ensure that triggers are effective and realistic. Lawmakers planned rate reductions more than a decade out; their triggers should reflect circumstances under which lawmakers would genuinely be comfortable making further cuts.

If reductions trigger at an inopportune time, future lawmakers could be placed in the unenviable position of canceling or even reversing a rate cut. Still worse, an ill-timed and unaffordable rate cut could undermine the state’s by then decades-long commitment to tax reform and tax relief. Future planned cuts could be scrapped and the reputation and staying power of existing reforms could be threatened. Proponents of future cuts should be wary of risking their many successes on ill-designed triggers, and cognizant of the degree to which certainty and stability are valued by individuals and businesses alike.

With adjustments to incorporate inflation and population growth into the trigger formulas, North Carolina policymakers can deliver on what the policy was always intended to do: implement further pro-growth rate reductions that run with, rather than ahead of, revenue availability.

About the Author: Jared Walczak is President of Walczak Policy Consulting and holds fellowships at multiple organizations, including the Tax Foundation, where he spent five years as Vice President of State Projects.